S&P/Experian: Auto Default Rate Registers Largest Increase Since December 2011

Despite the nine-basis-point increase, the auto loan default rate remains near levels recorded one year ago. However, declining auto sales and the normal end-of-year push to make room for newer models may encourage easier credit conditions and raise concerns about future defaults.

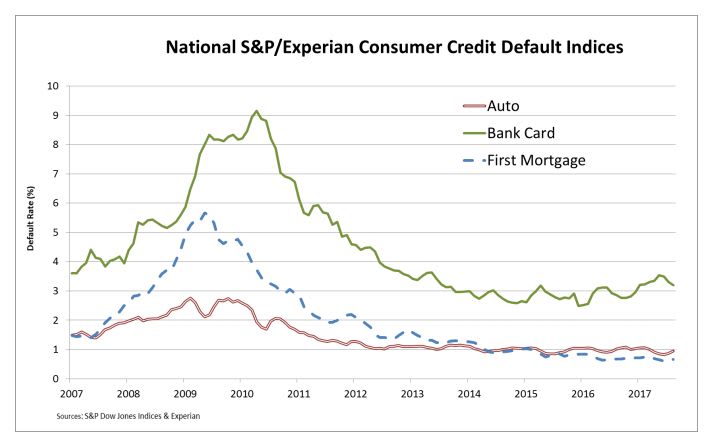

NEW YORK — Auto loan defaults in increased nine basis points from July to August, the largest month-over-month increase since December 2011, according to the S&P/Experian Consumer Credit Default Indices.

Despite the drop, the auto loan default rate remains low relative to historical levels. In fact, the rate is closer to levels recorded one year ago. The same is true for the composite rate for overall consumer defaults and first mortgage defaults, both of which increased three basis points from July.

“Overall, consumer credit defaults show no reason for alarm,” said David M. Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices. “Defaults on first mortgages are flat to down while defaults on auto loans have risen slightly in recent months. Consumer credit defaults on bank cards continue their upward creep since the end of 2015 despite a recent drop. The combination of an improving labor market, low inflation, and low interest rates are the principal factors behind currently favorable consumer credit conditions.”

The bank card default rate fell 12 basis points from July to 3.19% — the lowest level since December 2016. Bank cards were the only loan type to register a decrease in August.

Out of the five major cities analyzed by S&P/Experian, three registered increases in their default rates in August. New York recorded the largest increase, up 13 basis points from July to 0.95%. Los Angeles reported a rate of 0.66% for August, up three basis points from the previous month. Chicago came in at 0.94%, up four basis points from July.

Dallas reported a decrease of three basis points from the previous month to 0.74%, while Miami’s rate fell 10 basis points from July to 1.13%.

“Some future developments could affect consumer credit defaults: Auto sales have fallen since December 2016 and are down 11%. Declining auto sales and the normal end-of-model year push to make room for new cars may encourage easier credit conditions and raise concerns about future defaults,” Blitzer noted. “Hurricane damage in Houston and across Florida is creating substantial financial stress. The impact on mortgages on damaged or destroyed homes is not yet clear. Job losses and rising spending needs could lead to increased consumer credit defaults in coming months.”

Originally posted on F&I and Showroom

More Training

ASE Developing ADAS Calibration Credential

The National Institute of Automotive Excellence said its intent with the new technician program is to prioritize practical application and operational understanding over deep electrical diagnostics.

Read More →

Apply by March 31 for Automotive Scholarships

UAF is accepting applications for more than $900,000 in automotive and heavy-duty scholarships for the 2026-27 school year.

Read More →

Combatting the Technician Shortage

RockED and TruVideo have launched a free video inspection certification for automotive schools.

Read More →

The F&I Agent's Roadmap: Mastering the Cold In-Store Visit

Register for Allstate's FREE webinar on Oct. 21

Read More →

APCO Holdings Acquires DealerPRO Training

The addition expands company's footprint in fixed ops training

Read More →

Auto Dealership Training Program Expands

Protective Asset Protection offering is AI-driven.

Read More →

ASE Offers Free Vehicle-Fluids Webinar

Class will share updates on lubricant and filtration technologies in newer models.

Read More →

New ADAS Certification Announced

ASE training is intended to help service departments, shops optimize repair opportunities, customer confidence.

Read More →

ASE Offers Free Testing Webinar in Spanish

The class will give an overview of ASE testing in Spanish, including current tests, test development and test-preparation tools.

Read More →

F&I Conviction

It is not important that the client understands us – it is critical that they know we understand them!

Read More →